Learning to Spend Better by Caroline M. '18

This not a budgeting post.

This is not a post about budgeting, because no one likes to hear how to not spend their money.

I definitely didn’t, even when I really, really, needed to.

But I did learn to be spending better.

Being aware of what I spend on has helped me get more value from the things I have. Knowing makes me unafraid of “not having enough”, which then allows me to be more generous. And knowing gives me a lifestyle to work towards, one full of things that make me happy.

Because knowing how much I spend, lets me spend on the things that are actually important to me.

—

Knowing How Much You Spend

Keep track of what you spend, because chances are your guesstimate is wrong.

Every month up until my last semester, I was given a monthly allowance from my parents that was plenty for groceries, eating out, concerts, clothes, Ubers, and really anything else.

And I would tell myself, “I don’t spend that much”

As the month started to end, the account would decrease more rapidly too. I’d check the amount remaining and I would think, “Oh I have money left, I’m going to find something to use it on.”

My internet history was full of amazon doodads, my bookmarks full of wishlist items from forever21, and my fridge full of spoiling extra groceries.

Then the last week of the month would roll around and I would always be surprised at where all the money went. I may not have overdrafted many times, but I came dangerously close at least every other month.

But, “I don’t spend that much”.

I kept thinking that until someone I was seeing said to me, “I am worried about you, you really need to start budgeting” as he covered lunch for us again and my IOU tab grew. My partner before that had also begged me to save money, even if that meant I didn’t have to pay him back. RIP.

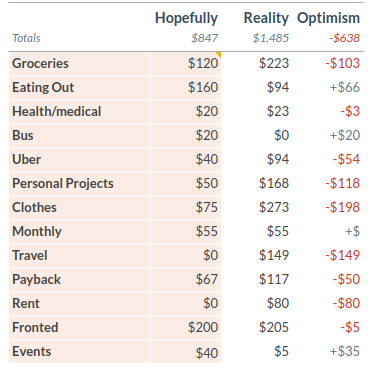

So finally, this past November, I started to keep track. I adapted a Google Sheets Monthly Budget template and started to log my purchases into the categories below. The first column was my initial estimate, with the second column the actual total of that category, and the third column the calculated difference.

I have a lot of optimism.

I have a lot of optimism.In my first attempt at estimating my expenses, I was off by over $100 for Groceries and off by over $50 for Uber, for a grand total of $638 off.

I learned that stuff adds up, really fast.

I realized that I could no longer lie to myself with the data right in front of me. I could no longer say to my mom, “No really I’m not spending that much, but please add more money (again).”

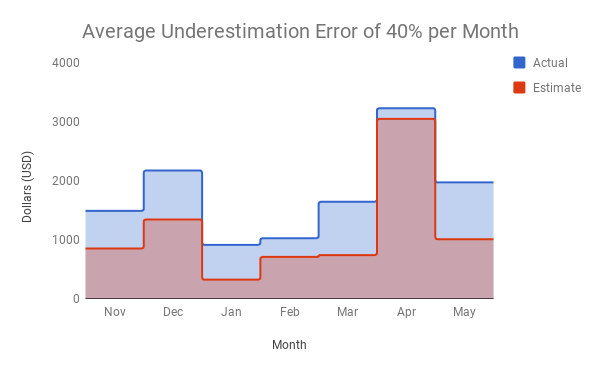

I continued to track my expenses, adjusting my expected budget to what I had spent in the previous month. And despite doing this for 8 months now, I’m still off by almost 40% when comparing the total estimated spending to actual spending.

Raw Estimation Error of Expenses by Month

Even after manually tracking expenses every month, I’m still surprised at how off I am at estimating what I spend. It also goes to show that I had no idea of how much and what I was spending on before tracking.

At least now I can see which categories I’m exceeding, which allows me to adjust my own expectation of what I actually spend and be more mindful the next month.

However, tracking expenses does take mental space and time to sit down and do it. (I don’t use Mint because it often miscategorizes my purchases, but that might save you manual input time)

What benefits are there to tracking, other than just knowing for the sake of knowing?

Just Knowing Can Decrease Your Spending

Being aware helps you make more intentional choices, which means less buying and more saving.

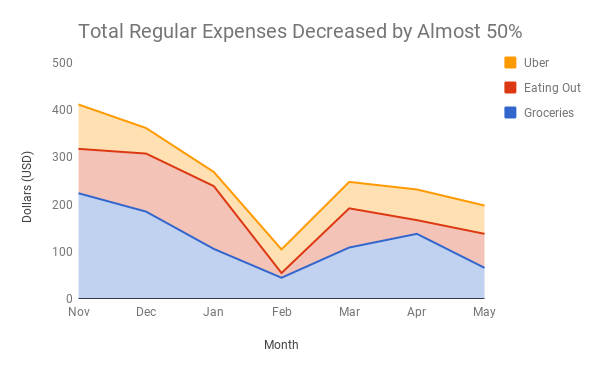

Being aware had a concrete affect on decreasing my spending amount. Over the months I kept track, there has been a consistent downwards trend of spending towards regular expenses, specifically Groceries, Eating Out, and Uber. Between November and May, this total decreased by almost 50% (noting that February’s drop was due to a specific event).

Raw Actual Expenses of Groceries, Eating Out, and Uber by Month

My total spending amount overall hasn’t really decreased, but by saving more in regular expenses, I have more for those regularly unexpected purchases (Yay more travel!).

Reducing these regular expenses also reduces waste. The amount of groceries and leftovers I throw away shows that I don’t need the amount I’m buying. And while the traffic in Boston will stay horrible, I can better do my part by defaulting to biking/skating/using public transit instead of Uber.

Knowing Gives You More Value From What You Have

Be careful of the new problems buying anything creates, otherwise you own items that give only one-time value versus the expected recurrent value over time.

Now that I was logging what I was spending on, I started to realize why I had so much random shit that I didn’t use.

Yoga mat, untouched for a year. Lipstick that’s been around… for a while and still very full. Outfits that I wore once, now crumpled in a corner.

At some point, I had poured many hours agonizing over which one had the better Amazon reviews, just to have the thing lying in my closet in a pile somewhere, unused.

When I realized that this repetitive cycle wasn’t making me happy, I changed how I bought things. Now I have a lot less clutter, and more importantly, a lot less guilt over having ‘wasted’ money.

My Method of Knowing What I Buy

- Want something? Put it in a category of how much I want it. For ex: “Really want”, “Considering”, “Never mind“.

- Next to the item, add a list of “problems it would solve” and potential “new problems“.

- If after that I decide to buy, add to end of “Definitely getting” list.

The act of listing helps me scratch that immediate “itch” of “I need something, but I’m not sure what it is.” It gives me an alternative when I’m pre-pset procrastinating, without buying anything thoughtlessly.

Having a time buffer is a test for if I actually want it or if this is just another “good idea to have” thing that I won’t end up using.

Sometimes the very next day, it will move from the “Considering” to “Never mind” list. Sometimes, I remember that I already have something that suffices. And it helps me understand that rewards aren’t actually rewards if I give them to myself every time I’m avoiding work.

And thinking about the new problems it might create is a self check-in of: would I be willing to put in the work or do I just want the “look of the lifestyle”?

*Cough Yoga Mats Cough*

Then when I do buy something, it’s not just for the sake of buying. I know that I’ll use it and it’ll make me happy, over and over again.

—

A few examples:

Red hair dye-

- “Considering“

- Problems it’d solve: Get reddish hair tips with black, looks really cool

- New Problems: Red hair dye fades fast for me, needs lots of maintenance so it ends up faded yellow-brown most of the time, stains tub, need to buy expensive bleach and deep conditioner

- Decision: One-time use, new problems not worth, don’t buy. Actually, my spiky black short hair is pretty cool already.

Dark Copper Red Lipstick-

- “Really Want”

- Problems it’d solve: specific matte rust nude color would look really, really good for everyday vs the deep red lipstick I have for special occasions

- New Problems: Very hard to wear without smudging, putting on in morning and touching up during day, lol rip kissing

- Decision: One-time use, new problems not worth, everyday lipstick not my thing, rock the deep red lipstick more if I feel like it.

Chrome Bravo 2.0 Backpack-

- “Definitely getting”

- Problems it’d solve: more space for lunch, more padding for long city travel, outside strap for skates, look of urban traveler

- New Problems: kinda big

- Decision: Buy, will use and is versatile for many settings like school, travel, and skating

—

This habit of knowing and intentional buying has also helped me a ton with my ADHD and buying impulsivity. By creating a habit I’m pre-committed to, I rely less on the in-the-moment willpower, that when I’m tired, sad, and stressed, I definitely don’t have.

So now when I buy with this habit of process, I end up with a lot less guilt and shame. Building that trust in myself to let myself spend has been worth every single in-the-moment buy that I didn’t end up making.

Knowing You Have Enough Makes It Comfortable to Give

Budgeting for generosity helps actual follow through

There was this video game convention that I was going to and when I asked another friend if he was going, this is what I remember him saying.

“I really fucked up, every year my nephew and I usually go but last year I was broke and so I promised him we’d go this year. But I really messed up again and didn’t plan for it. He was really looking forward to it too and we don’t get to spend much time together.”

At that moment, I so wished that I hadn’t burned through all my money so soon. I wanted so badly to be able to give him and his nephew this experience, especially since I’m relatively less financially insecure.

But at the time I had no idea of what I might need in the near future.

I didn’t want to put myself in a bind and ‘not have enough’. I felt like I just ‘didn’t have enough’ to give because I wasn’t sure how much I had or would need. I felt guilty and sad for missing this opportunity to give a friend quality time with his family.

Next time, I won’t be making the same mistake.

Because I keep track of what I spend, I know how much is left. Even though I’m still bad at estimating what I’ll spend every month, I have a much better idea of what it is consistently and therefore feel more secure.

I also put these kinds of gifts in a new budget category called “Friends”, so I don’t need to be afraid of the slippery slope “well I can’t give to everyone so I’m not going to give” because I’m keeping track.

I know that giving to friends is really important to me, so I want to make sure I actually do it and also plan for it.

This semester, I was able to contribute to another friend’s last-minute need to hire a thesis editor in order to graduate. I was also able to compensate a friend for crash coursing me in 6.046 tutoring when I really needed it the night before, even if I knew they’d be willing to help me anyway.

They’re both people that are really important to me, and it makes me incredibly happy knowing that I can help them.

If I’m bottoming out at the end of every month, they wouldn’t have accepted my money because they would know I’d ‘need’ it. I also would be afraid of putting myself in a pinch and regretting giving later, which is the worst.

This certainty of “I know I have enough” also extends to beyond friends. If I’m stuck in an Uber because of traffic, I think that time should be compensated, so I tip. I can live by my values a little closer. My next goal is to set aside $1/month for giving to homeless people I run into, gradually increasing it.

Giving is deeply fulfilling to me, and actually giving with the security that I have enough, even more so.

Knowing Helps You Afford the Lifestyle You Want

Knowing how much things that make you happy cost makes it easier to see real success.

I just graduated, and I’m looking for a J.E.R.B. (Just Employ-me Really Broke)

But how broke?

Okay, actually I’m not going to be that broke.

Here’s a rough month breakdown:

Rent: $600 (splitting a room)

Living Expenses: $500 (upper bound, extrapolated)

Loans: $150 (upper bound, $0 for the next 6 months)

Total per month estimate: $1,250 / month

That means with my current savings, I have about 2 months of lead time if I can’t find a job. In addition to the 2 months that will be all-expenses paid with this program in Japan, I have some time to find something.

But what would be the ideal salary?

Before MIT, I had this idea, that I suspect is more widespread than admitted, that making ~$100k = success. That the six-figure salary was equivalent to “you’re doing something useful for society”.

But I value leisure over consumption by a lot.

I like waking up late. I like working with people to improve the community. I like skating with friends in different cities and couchsurfing with them. I like cooking for myself and living simply. I like not needing to dress in formal every day. I like having the mental energy and time to write blogs like this.

And I need quality time with quality friends.

In my current lifestyle, I am doing all of that. If I need a total of $1,250 / month, a job that pays me about $18/hr that I can work for about 20 hrs/week, gets me to $1,440 / month.

The yearly salary for that comes out to be about $20,000, approximately rounded up for taxes and some buffer because I’m too lazy to do the real math. #EconIsNotFinance

It’s likely I won’t be working just 20hrs/week, but if that’s all I need to keep this lifestyle that has the flexibility I need right now, I have a lot less stress about getting a J.E.R.B.

Knowing these numbers also lets me entertain crazy ideas like potentially starting a Patreon to write blogs full-time, because that would be super fucking awesome. I would know how many people with $x of contribution I’d need to make it a sustainable lifestyle.

Knowing these could even be remotely options makes finding a job so much more exciting and full of possibilities. I can plan and set goals and even stretch goals. I could start a savings account *gasp*.

I feel self-sufficient and it feels a lot more possible to make real choices for my life. I have something really great to look forward to, and that’s freedom.

—

I wish I had this for myself freshman year, to help me understand why it’s important to be paying attention to my spending. I might even have ended up saving more as a result, which would’ve given me more runway and flexibility than I have now.

But these past few years, I’ve been learning a lot about what works and doesn’t work for me, like cooking for myself, living off campus, and now how to spend better. I’m happy where I am, because even if I can’t start over with things I wish I’d known, I’m still rewriting the ending.

I really am more content with these things that give me real value. I am more certain that I have enough, and I am so grateful to be in a position where I can help those who have less. I am empowered by knowing what I have to look forward to and how I could get there.

And it all started because of an awkward lunch date and someone important to me saying, “Get your shit together Caroline.”

Getting my shit together looks like spending on things that are actually important to me, and I think I’m getting there.

– – – – – – – – – –

If you’re convinced that you should know what you spend, here are a few things to help you start:

- The excel I used can be found as “Monthly Budget” in google sheets templates

- Mint is a money tracking app that I know some people use

- You Need a Budget is also an excellent proactive money planning app

*This list is very short because this post was not intended as a concrete recommendation source, there are plenty out there. This was written in hopes of sharing my journey of realizing why doing this at all, is important.

**Also shout out to 15.276, Communicating With Data, for teaching me how to make fun, easy-to-read graphs that get the point across

As always, feel free to share thoughts to me at [email protected] (with a +/- week of lag response time because I will be traveling soon)

Cross-posted on medium.